AdRoll vs. The Trade Desk: Comparing Pricing, Features, and Benefits of Two Top DSPs

AdRoll and the Trade Desk compete head-to-head on many features. Our guide covers DTC advertising, ecommerce, ABM, privacy, channel coverage, and pricing.

Read More

Major disruptions have a tendency of sparking and nurturing innovation. Take, for example, the explosion in disruptive startups that happened after the Great Recession. The period immediately after the market collapse gave us Uber and Lyft, Snapchat and Instagram, Airbnb, and countless other companies that have changed the way we work and play. It was also the age of major growth for Facebook, Twitter, and Amazon. A disruption in the way the world works opens the door for brands that want to disrupt the way we do other, more mundane day-to-day activities.

Prior to COVID-19, a wave of financial technology companies (often grouped under the shorthand of “FinTech”) was making quiet progress changing the way consumers interact with money. The FinTech trend isn’t new — many of the biggest names like LendingTree come from the first wave of startups from the 1990s, many more like Mint.com and CreditKarma come from the second dot-com wave of the 2000s.

But the late 20-teens saw an acceleration and blossoming that moved FinTech past the “matchmaking” style of previous iterations and into a new paradigm: true financial service companies selling financial products directly to retail consumers, but living entirely online. Growing out of the direct-to-consumer (D2C) revolution, this new wave adopted the parts of D2C brands that consumers loved and adapted them to banking, insurance, and even complex financial instruments.

That blossoming turned into a tsunami as COVID-19 hit. Much of the world was, and many parts remain, under various lockdown, quarantine, and shelter-in-place orders. Businesses have closed their doors, sometimes until COVID is over and sometimes for good, leading to ripple effects throughout the economy. Unemployment spiked to an unprecedented high, and the very idea of work is being reexamined.

John F. Kennedy is credited with popularizing the quote, “In the Chinese language, the word ‘crisis’ is composed of two characters, one representing danger and the other, opportunity.” That perfectly describes the current confluence of crises — there is danger, and a real human cost to the events going on, but they also represent an opportunity for financial companies to radically change the way people bank, save, invest, insure, and plan their financial futures.

And for many FinTech firms, this is an opportunity to make the world a better place — helping the unbanked and underbanked get access to financial services, increasing the information available to retail consumers, and finding ways to provide a safety net to people in danger of falling through the cracks. These are the stories of three FinTech companies that have found a way to grow, before, during, and after COVID-19.

According to Forbes, about 35% of the U.S. workforce does some freelance work. 28% of those freelancers do so full time, and that percentage is growing yearly. It’s no exaggeration to say that for many Americans, the nature of work is changing. Just over the last few decades, we’ve seen two radical transformations in what “having a career” means: from working with one company your whole life, to the job-hopping and uncertainty of the 1990s and 2000s, to the modern notion of the gig economy.

So with all of these massive changes, it seems odd that our idea of workplace benefits and financial support services still very much cater to a pre-1990s idea of work. Catch is a portable personal benefits company that set out to modernize how people deal with the finances of having a job. Their platform helps contractors, freelancers, and other various gig workers do the things that traditional employees take for granted. Things like tax withholding, buying insurance, retirement savings and investment, and vacation time planning.

Unlike traditional benefits providers, which are contracted by companies on behalf of their employees, Catch works with individual freelancers to provide them with some of the stability that most workers take for granted. Kristen Anderson, Catch’s CEO, talks a lot about that stability, especially in the historical context of the 1918 flu pandemic.

“There was massive demand for really stable jobs; people prioritized factory jobs and union jobs. They wanted stability. And into the Great Depression, people still valued stability over wealth by a long shot,” explains Kristen. “We now have a chance to say, ‘Okay, how do we create financial stability, given this context?’ Crises like the pandemic in 1918 and the pandemic now in 2020 give us an opportunity to ask, ‘What kind of world do we want to create in terms of the stability and welfare we provide for our people?’”

Finding ways to bring that stability is complicated by the wide range of people that Catch serves. “I think the biggest challenge is that our user base is extremely diverse, so their experience through this pandemic has been really diverse,” says Kristen. “Some are hairstylists who haven't been able to take on a job in 60 days. Some are UX/UI designers whose work hasn't been affected at all. Some folks have small kids so everything's crazy for them, and other folks are sort of by themselves and dealing with loneliness.

“I think this range of experiences means it's really hard to hit the right tone, what with all of those different emotions layered onto what’s a pretty difficult situation,” adds Kristen. So with so many different ships weathering the same storm, how is Catch addressing the disconnect?

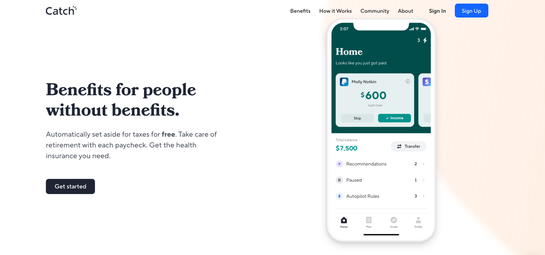

Image: Catch

When crises hit, consumers often reevaluate their priorities. This can be changing the categories they spend money on, prioritizing savings over spending, donating more to charity, or pulling back from the commercial space altogether.

For Catch, it meant recognizing that some of their traditional messaging was no longer appropriate. Prior to COVID-19, much of their ad strategy focused on the typical financial selling points of long-term growth, returns on investment, future planning, and similar. This became problematic as the unemployment rate soared and millions of people began worrying about tomorrow rather than 30 years down the line. In mid-March, Catch turned off their re-engagement campaigns for consumers that entered their funnel but hadn’t yet fully onboarded.

“We realized some of those campaigns were a little bit tone-deaf in the context of folks not being able to work,” explains Kristen. “We had a great campaign around things like, 'Make sure you're setting aside for the future' and 'Save for your future self'. That sort of messaging felt really off-putting in a time when some folks don't have enough income to pay for their meals or rent. We decided it wasn't worth any additional conversion because of how that messaging might be perceived.”

A recent COVID-19 report by market researchers FMCG Gurus found that: “Consumers want brands to demonstrate they have the best interests of the individual and wider society at heart and are not just driven by the desire for profit maximization. As such, they will seek out brands that they believe demonstrate traits such as kindness, empathy, and compassion.”

Catch recognized early that any marginal customer growth today could lead to serious damage for the brand tomorrow. Instead, the brand decided that being a responsible and caring member of the freelancer community was more important to their long-term goals. They’ve adapted their tracking metrics to keep with their new focus, too.

“We've really tried to focus on intent rather than typical metrics,” Kristen explains. “Obviously, the thing that's really important for a business’ success is revenue unit economics, profitability, etc. But in the interim, things like: Do people still feel like they need this product? Are they engaging with it? Are they marking their income even if they're not withholding? We also give them the option to skip this if they don't want to set aside any money right now because times are tough.

“We’re also seeing certain metrics going up really quickly, like health insurance, with the levels of unemployment that we're seeing there's a much larger need for people to get independent health insurance,” adds Kristen.

Along with shifting priorities in messaging and metrics, brands reacting to unexpected changes have been forced to change what they offer consumers. And while emergencies tend to force pivots, the ability to do so is critically important for any brand that is trying to grow.

Catch recognized early that there were a few things they could do differently to better serve their customers. One of the first ones launched was a new emergency savings feature. Kristen explains, “Emergency savings isn't exactly a part of that traditional benefits world, but it was something that we felt was just really important to get live right now because people were paying much closer attention to it. The recency and severity of this crisis are really at the top of their minds right now when they're thinking about protecting their financial futures.”

But the shift went beyond just offering new services that matched the times. It also meant changing up their marketing to focus more on offering education: how to get through the pandemic, how to prepare for crises, how to find stability in a changing world.

“I think in terms of our users, if we’d known what was coming we would have tried to help prepare the educational content a little bit earlier,” Kristen says. “We would've focused on bringing together really rich and helpful content early and making sure that our go-to-market reflected that people weren't going to be going outside of their homes.”

In traditional growth-hacking culture, there is a belief that a pivot means big changes to the core functionality of the product. Instagram, for example, famously pivoted from being a review service like Yelp to the image-sharing platform and social network we know and love today. But a pivot can be so much more. It could be an additional service that expands a product to fit the times. Or it can be a temporary change in focus from selling to education, offering content as the primary service while market conditions shift.

Fast-growing businesses need to understand and embrace the pivot in all of its many forms. Market conditions change quickly, and a brand that can react to them will always outgrow a brand that can’t. At the same time, brands need to make sure that they have the discipline to not overcorrect — sometimes the best pivot is one that enhances the core experience, rather than changing it completely.

On the history of the benefits system:

[playlist tracklist="false" artists="false" ids="4868"]

KPIs should never be seen as sacred cows. Instead of static metrics that are immutable and unchanging, make sure that they are regularly reevaluated to fit the situation your business is in right now and in the future, not where it was six months ago.

Check your messaging regularly, and update as needed. Not every campaign can, or should, be run in every kind of market condition.

Don’t be afraid to pivot, but also realize that a pivot doesn’t have to be a complete 180 — small changes that shift your business slightly but significantly are also important.

A decade ago, cryptocurrency was something reserved for quiet computer enthusiasts — a secret world that most people barely knew existed. Over the last couple of years, a highly- publicized period of exponential growth, followed by a spectacular implosion, brought crypto into the mainstream. Bitcoin’s rise to a value of $20,000 per made it so popular, it was covered on the evening news. Little old ladies were buying Bitcoin, and giving it to their grandchildren as birthday and Christmas presents. It was ubiquitous in the national consciousness.

But despite this colossal rise in awareness, getting and using cryptocurrency remains difficult. Even tech-savvy crypto investors often find themselves locked out of many commonplace financial transactions. Take, for example, something as simple as getting a loan. For a variety of reasons, many banks won’t accept Bitcoin and the like as collateral.

Enter SALT, a FinTech company that accepts various common cryptocurrencies to secure loans for clients. Since SALT was built from the ground up to handle exactly this kind of lending, it was able to mitigate some of the issues that traditional banks have in dealing with cryptocurrency assets — issues like dynamic valuations, the difficulty of securing the collateral, and just not having a full understanding of the assets.

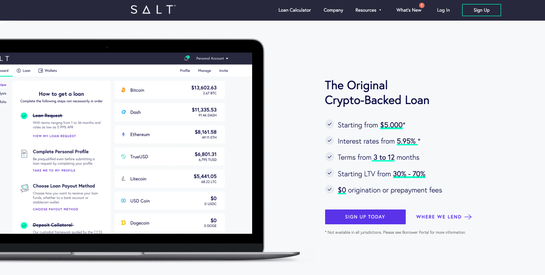

Image: SALT

One of the first problems SALT needed to address was how to build their platform. Cryptocurrency is hardly new technology — the “ledger,” the recorded history of every Bitcoin transaction ever made, started in January of 2009. Since then, many intrepid tech pioneers have built up a wide array of cryptocurrency tools. These ranged from basic necessities like software to store and track your crypto hoard, called “wallets”, all the way up to complex exchange markets and even physical ATMs that would allow you to buy and sell Bitcoin or trade it for cash.

With so many pieces already built, it seemed wasteful for SALT to start from scratch. Before a single line of code was written, the conversation quickly became, “What do we need to reproduce ourselves, and what can we plug-in from ready-made code?”

This is a vital discussion for any startup, whether physical or digital, and one that often gets swept under the rug or not had at all. It goes beyond just which pieces of software to include in a product, and speaks to a more important conversation: how much expertise should be grown organically, and how much should be brought in from outside?

SALT ultimately decided that they would be stronger as a company building that expertise, and large parts of their application, internally. “We spent time early on educating ourselves via a book club to get lessons in mathematics. It helped us figure out how to sew that into the product we were building. Our whole ethos is really baked in this now — developer-oriented, ideology focused, curious,” says SALT’s Co-President and CPO, Rob Odell.

Not every company will be able to do that, though, and certainly not at every life stage it passes through. Starting these kinds of conversations early can mean the difference between a company that has a clear purpose and can grow without getting in its own way, and a company that constantly fights itself to get to the next milestone.

It should not come as a surprise that cryptocurrencies, like many speculative instruments, have attracted their fair share of grifters, con men, tricksters, and scam artists. As a result of some high-profile scams, many traditional advertising and marketing channels have come down hard on companies dealing with digital currency. Google requires all cryptocurrency services advertising on their platform to be certified. Twitter has made a habit of shadowbanning accounts that talk about cryptocurrency.

All of this makes it difficult to advertise and promote a new service. Especially a financial service, where trust is key to success, and where visibility is often used as a shorthand to estimate trust. For a service like SALT, just starting out and needing to validate itself before people trust it with their money, this was a problem that needed a creative solution.

“Building that level of trust early on was hard,” admits Rob. “So we decided to let people deposit their assets with us and never moved them. They could go anywhere and see they were sitting with us, that was a big differentiator for us because people felt comfortable. We worked to build trust around that.”

The company also looked for alternate ways to reach their audience — going to meetups and networking groups, finding public and private Slack channels for crypto enthusiasts, attending conferences. The strategy paid off. When COVID-19 hit, the company was well-positioned to survive through the crisis. In fact, they were in a position to come out of it even stronger.

“Most crypto companies are doing well in general since none of them have had to rely on physical contact with customers. We were kind of already set up for remote work, so it was a shift but it wasn’t detrimental,” says Rob. “Our community is very passionate and COVID-19 has created more interest in crypto — people are rallying around the idea and thinking of getting involved. There’s more of a spotlight on its value as an alternative. It’s been very validating for the community.”

The age of digital marketing has made reaching an audience as simple as clicking a button for many brands. But that ease of use often hides an important truth: these are not the only channels available to high-growth brands, nor should they be the only ones under consideration. Focusing entirely on standard digital advertising channels risks blinding brand builders from the many alternatives that exist, many of which can have a much higher ROI.

On how to bring value to the community:

[playlist tracklist="false" artists="false" ids="4869"]

Don’t assume everything needs to be scratch-built. There’s no shame in taking commonly-existing frameworks, plugins, scripts, and bits of code and repurposing them for what you need.

Remember that there was marketing before digital. Don’t be spoiled by easy clicks with CPC and social ads — building communities works, is cost-effective, and helps growing brands stand out.

The best marketing in the world won’t be able to overcome trust issues. Especially for financial companies. Build trust in whatever way suits your brand best, and the rest will come naturally.

Property insurance is an old industry — the basic property insurance policies can be traced back to the 1660s, to the Great Fire of London that destroyed over 13,000 homes. The first fire insurance company, the Insurance Office for Houses, was established in 1681 at the back of the Royal Exchange, and insured brick and frame homes. Of course, the market has changed a little since then — you can now insure all manner of homes, not just brick and frame. But by and large, the industry hasn’t changed much since those early days.

“Until recently, home insurance had not changed in 150 years. So I do think that it was ripe for disruption,” says VP of Marketing for Hippo, Andrea Collins.

Of course with an industry this old, the real question isn’t, “Is there room for disruption?” The question is, “Where should we start?” The digital revolution has done a lot for the insurance field, from bringing the application process online to making claims faster and easier. But a lot of the changes so far have been on the surface. Companies have moved online to make communication easier, but few have really rethought what insurance could be in a digital age.

Hippo changed that by starting where most online insurance companies ended. The company offers fast quoting and policy writing — 60 seconds and four minutes, respectively. And they offer the convenience of digital policy writing and single-touch claim processing. But Andrea doesn’t see these as the only selling points.

“It's about being there during your customers' time of need and providing a seamless claims experience while making sure there's also empathy factored in,” she says. “We have a claims concierge team, which provides one point of contact for the customer from the start of a claim, all the way through to its resolution.”

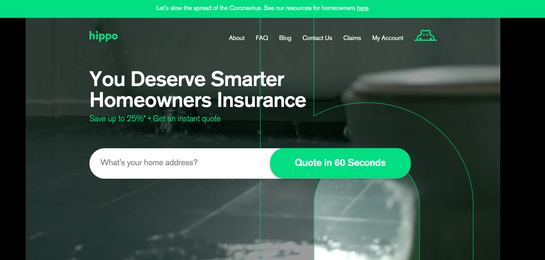

Image: Hippo

Disruption comes in waves. The first wave in the 1990s followed a simple formula: take what people already do, but move it online. The ill-fated Pets.com took pet stores and moved them online. Amazon did the same with books, albeit more successfully. The second wave was the web 2.0 revolution that brought us social networks. It was disruptive, but it really was just changing the way we communicate, rather than the way we understand brands. The third wave is where things started getting interesting.

Hippo comes in during this third wave of digital disruption — the one where companies are doing more than finding new ways to communicate with consumers, but are actually using the technology tools available to them to rethink the way traditional businesses work. Instead of thinking about insurance as simply a policy that is sold to a consumer and forgotten about unless something happened, they started with the idea that it might be possible to use technology to actually help consumers get more benefits from their insurer. That started by examining what modern policies actually needed.

“The majority of home insurance policies include coverage for fur coats and pewter bowls, while only covering about $2,000 for their electronics,” Andrea explains about traditional home insurance policies. “That is why it is so important for us to add in the right amount of coverage by understanding the customer first. For example, just knowing that many people carry $2,000 of electronics in their pockets when they leave the office means we need more coverage in this area. It starts with asking what people actually need from their home insurance, what do people actually own in their homes, and how can we properly cover these items so that people can have the right amount of coverage to protect themselves and their properties?”

Then on top of rethinking what is protected and how Hippo focused on finding ways to actually decrease the number of claims that are submitted by decreasing the losses customers suffered. That started with a smart home device kit that the company provides to customers that would educate them on how to best protect themselves and alert them to issues in their home. Unlike many other companies that have similar approaches, Hippo doesn’t use this device to gather data or spy on consumers. Instead, they found that just giving customers the information they needed to make better decisions they could reduce the number of claims they were paying out.

Disruption gets talked about often enough that it has largely become a buzzword. Every company is disrupting something, at all times. But real industry disruption isn’t just changing the mechanics of how an industry sells its products. Disrupting insurance isn’t just “insurance sales, but online.” Instead, it’s about rethinking the way brands provide value to customers. Hippo doesn’t just sell insurance over the net, they are changing the underlying assumptions that go into providing insurance.

Part of the key differentiator Hippo provides is integrating a home maintenance plan into their offering. What Hippo found was that customers were treating a lot of their maintenance as just another to-do on a long list of to-dos. Most weren’t thinking about, as Andrea says, how a clogged dryer vent wasn’t just a chore but a potential fire hazard. By partnering, and eventually acquiring, a home maintenance service, Hippo was able to not just disrupt consumer expectations on what home insurance could be, but make those consumers safer and improve their own bottom line by minimizing the risk of needing to pay out a claim.

When COVID-19 hit, they took this approach a step further. With in-home maintenance being much more restricted, they brought their service online. Customers that were having issues could request a virtual appointment through the website, and a highly-qualified contractor would get on the phone with them and help them troubleshoot basic problems. Then, they took it another step further and opened up their service, for free, to everyone in the U.S.

“There were a lot of appliances breaking because you're using your dishwasher four times more per week than you used to, and your clothes dryer twice as much, and all of those things just are not meant to be used as frequently. So we created a virtual product that tied into the need there,” Andrea said.

The virtual checkup was a hit, and a huge point of differentiation from what competitors were doing because it spoke to a real need that consumers had, but maybe didn’t realize they had. One of the strengths of a true digital disruptor is their ability to think not about how to take what’s already there and do it better, but to imagine what things could be like in an ideal world.

Disrupting an industry needs to be deeper than just moving it online. Instead, consider new options opened by digital commerce and build from that as a starting point.

Growing isn’t just about increasing revenues. Sometimes, decreasing costs is even more important. Always look for opportunities to shrink outlays in innovative ways.

World-conquering companies don’t just do things a little better. They change the game entirely. Don’t just try to incrementally improve on competitors — look for ways to lap them entirely.

The thread that runs through the FinTech companies profiled here, and the FinTech companies that are poised to be the big household names of tomorrow, is that they think about the products and services they offer in a new way. Catch created a suite of products for workers in the new economy. SALT has built a platform for financing purchases with a new currency. Hippo has moved home insurance into new product offerings. And they’ve found success by betting on the next big thing, not the last big thing.

As COVID-19 threatens to reshape society, the economy, and governance, winning financial technology companies will need to ask themselves: are we solving yesterday’s problems, or tomorrow’s? That might seem like a trite way to think about it; after all, every tech company thinks that they’re disrupting an industry. But the companies that come out of this crisis stronger than before will be the ones that have really dug deep and focused on that future need.

They’ll also be the companies that have a deep understanding of who they are selling to, and how to approach them in a respectful and empathic way. The consumers of tomorrow, dealing with the aftermath of a global change and an unprecedented number of unemployed and struggling friends and neighbors, may not be as interested in boastful marketing. The financial firm of the future will need to do better than promising great returns. They’ll need to promise greater good for everyone.

FinTech companies that manage to nail both of these, solving emergent problems and doing so in a way that benefits society, will be the FinTech companies that win. The companies that focus on Gordon Gecko’s infamous “greed is good” approach, on the other hand, will be left behind in the dustbins of history.

Last updated on April 22nd, 2026.