AdRoll vs. The Trade Desk: Comparing Pricing, Features, and Benefits of Two Top DSPs

AdRoll and the Trade Desk compete head-to-head on many features. Our guide covers DTC advertising, ecommerce, ABM, privacy, channel coverage, and pricing.

Read More

Quick survey: When was the last time you physically went to a bank to do multiple transactions? While traditional banking won’t be going anywhere soon — after all, people still need to speak to customer representatives for dozens of transaction types, inquiries, and concerns — there’s no doubting the changes we’ve seen in the banking sector.

Chances are, you’re part of the majority of people who’ve made the switch to online banking and mobile. And when just about everybody owns a smartphone in this day and age, mobile experiences have become especially important. JPMorgan Chase & Co. CEO of Consumer Lending, Marianne Lake, has even gone to claim that over half of millennials are willing to switch banks if it meant better mobile experiences.

Fortunately, excellent mobile experiences are possible and they're getting better all the time. Recent and rapid developments in the fintech industry, such as the rise of jQuery and blockchain, have paved the way for faster, more secure online banking, even from mobile devices.

But how exactly is mobile changing the banking industry? And is there something we can learn?

Let’s dive into the changes we see in the banking sector brought about by mobile developments. And because digital is evening out the playing field for several players, let’s also explore what makes mobile banking apps as successful as they are when it comes to customer loyalty and experiences.

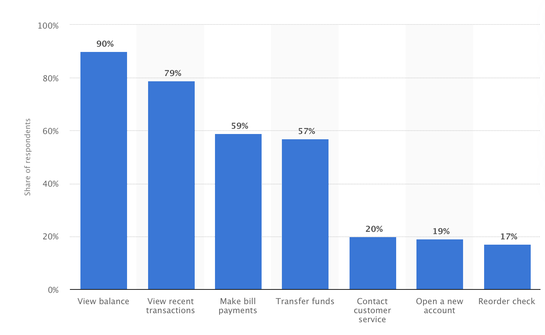

Today, about 59% of Americans say they use mobile banking to pay their bills aside from more popular use cases like checking balances and looking at recent transactions. People also used to do these tasks on banking websites, but more and more people prefer to do them on apps.

Image: Statista

Need to make a payment at your favorite café? Check if they process payments through Apple Pay or other digital wallets. Several banking apps are making it easier to send and receive payments for different products and services, and not just for online purchases.

Today, it’s more than possible to leave your home without cash in your wallet – your smartphone is more than enough.

This is a feature we can expect to see more banks roll out to their mobile apps. And if you’re worried about the security for cardless ATM withdrawals, know that these banking apps will probably make withdrawing cash more secure.

In the past, someone only needed your card and PIN to steal money from the ATM. In the future, we’ll be seeing more banks use a combination of biometrics and passwords in conjunction with your PIN.

Even if someone steals your phone, they’ll be required to go through several high-security layers (instead of just your PIN) before they can withdraw cash from an ATM.

Chase Bank is already rolling out these features, so we can only expect more banks to follow.

Gone are the days when you could only make investments through a broker. Today, the demand for more accessible investing and trading is being met by many a mobile app. You can trade stocks, mutual funds, ETFs, and bonds without speaking to anyone at the bank or paying hefty trading fees.

Platforms like Robinhood were some of the first to arrive on the investing app scene, but they are quickly being overshadowed by newer players, like Ally, for having better track records.

Banking-as-a-Service (BaaS) means financial institutions are providing more solutions and services that extend beyond the four walls of a bank. Many banks can scale their operations and cater to more of their customers’ needs by introducing functionality and convenience you can only get from a mobile app.

Traditional banking institutions aren’t the only ones rolling out apps in the fintech space. We mentioned Ally and Robinhood as examples in the investing space, but we also see a rise in institution-less banks.

Take PayPal and Apple Pay, for example. These two apps and services have no brick-and-mortar banking space yet share services and features you might get from a typical bank, including holding liquid cash and sending and receiving money.

As technology develops, we can only imagine what the future of banking will look like. In the meantime, let’s take a look at what these top banking apps are doing to keep customers happy and loyal when they’re surrounded by a sea of competition.

The top banking apps understand their customers’ needs, enough that they’ve been able to change their behavior. When consumers needed faster ways to make a transaction, banking apps included online money transfers in their system. When consumers wanted to manage their loans without speaking to their bank manager, banks like Capital One delivered.

And more than just new features on their apps, top banking apps know how to nurture their relationships with customers. RBS Citizens, for example, used data from customer panels to find out which banking features their consumers used most from their competitors. They then used this data to develop their first mobile app version — that’s one of the highest-rated on the App Store.

For more on creating customer delight:

Many banking apps are going above and beyond by introducing features customers didn’t have in traditional banks. Simple, for example, has a Safe to Spend feature unique to it that shows people whether they have the expendable income for a planned expense. Meanwhile, USAA was the first to introduce face and voice recognition for logging in to your account.

Even if you aren’t in the fintech industry, this shows us the power of marrying the sincere goal that is helping your customers with the unique added convenience and features you get from technology.

Even before mobile banking rose to popularity, many banks were already rewarding loyal customers. But with mobile apps, many banks are taking their rewards programs to the next level. Just look at the Bank of America, which now includes its Bank AmeriDeals – where customers can find exclusive merchant discounts and cashback – right from the app.

For more on loyalty programs:

Last but not least, privacy is a huge concern among any business, especially for fintech. Amid all kinds of scams, attacks, and scandals, people now more than ever want to know how companies are using their data.

You don’t have to be in financial services to know that you ought to protect your and your customers’ data. And while it isn’t required, one of the best things you can do is telling customers exactly how you’re keeping their data safe.

We see banking apps emphasize their data encryption, introducing easy-to-use safety and anti-hacking features, as well as clearly communicating service downtimes and disruptions.

Technology is changing the way we use and interact with banks, and financial institutions are helping bridge the gap further by introducing and improving mobile apps. We can pick up a few key lessons by looking at how these institutions are adapting their operations to meet a mobile-first need, putting their customer experiences and needs at the forefront of their business.

Last updated on May 1st, 2026.